The buffet analogy

It’s like settling down to indulge at a buffet. Obviously, there’s often lots of good food at a buffet. Been to one of those in the Drakensberg, in one of those fancy hotels? You have to be a real foodie to enjoy a buffet; otherwise, you’ll leave pretty full and requiring Eno or Gaviscon.

Ever gone to a Christmas lunch feeling festive and left feeling sick after overstuffing yourself? That’s how over-diversification feels to your portfolio.

Ever gone to a buffet and eaten too many carbs rice, potatoes, or bread and then been unable to enjoy the delicate meats? That’s over-diversification again.

The old saying says it well: “Don’t put all your eggs in one basket.” I suppose you could trip and break them all. Unless your eggs are boiled, don’t keep them together they’ll rattle against each other, and you could lose them all.

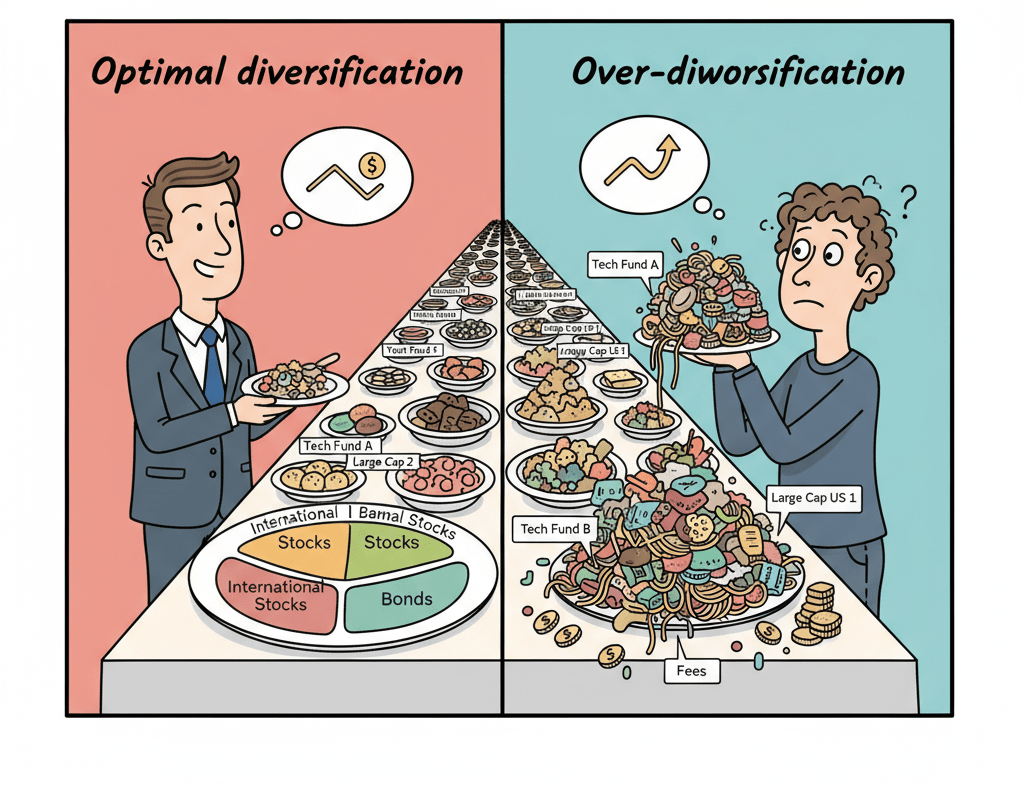

Finding the sweet spot

In my opinion, one needs at least one JSE Top 40 ETF and another global version like the MSCI World Index or S&P 500 ETF, or perhaps even a developing world ETF if you believe in the new world order.

Just be careful too many ETFs might result in duplication of the same shares, defeating the wisdom of diversification. You could also end up paying more in fees for the same basket of shares.

There are so many good ETFs out there (spoiler alert), but you can’t hold them all. Choose what works for you have your own tailor-made strategy.

If you go for a buffet, remember: too much good food can make you sick, too. Be picky about what you eat you can’t eat every dish.

Personally, I often start with new dishes I’ve never tried before, since it’s like an adventure for me. Just don’t do the same with your investments.

Most times, the same old tried-and-tested JSE Top 40 or S&P 500 is your good old lamb or beef roast you can never go wrong with these if you’re planning to hold them for decades.

Investing is a long-term meal

If you’re investing in shares, you should hold them for decades anyway. Pulling out, chopping, and changing often is the guaranteed way to lose your money, since no one is good at timing the market. Instead, spend time in the market.

At times, it’s even important at a buffet to walk around and eat with your eyes before choosing which food to try. It’s the same with investments there are fees involved, so do some homework. Pull out the fund fact sheet, check performance, and most importantly, the risk profile as well.

Just don’t do too much homework, since time is not always on your side in the investment world.

Particularly if you’re like me I’m in my early 40s time is flying, and I need that money in the market ASAP so I can catch the compounding snowball before summer kicks in and risk snow melting away.

Diversification is like a wardrobe

Another way to think of diversification is as a wardrobe with all-season clothes.

It’s spring here in Durban, and if you don’t have slip-ons in your cupboard, you’d better get some the humidity of summer is just around the corner.

Not sure if there’s anyone in Durban without slip-ons, or perhaps I should say Crocs. They’re pretty useful with socks in winter here, since we have warm winters. When summer starts, you take off the socks and you’re ready for uShaka Marine World in your Crocs.

Sounds weird to say “warm winters”? Ask the Jozi dudes they’ll tell you what winter really is in Gauteng. Crocs and socks won’t work inland at 5 a.m. during peak winter.

Back to investing, diversification is meant to spread your risk across funds, asset classes, and geography that is, local and offshore.

Asset classes and modern investing

Talking about asset classes it’s almost crazy not to own some crypto in your portfolio.

I’ve been pretty slow in that regard; being a bit rigid didn’t help or perhaps I should say old school. It’s high time I purchase some crypto, just in case.

Not sure about gold, though prices have been super crazy of late. I’ve even been tempted to buy a pick and explore Jozi one of these days!

Talking of gold, retirement funds are like gold to your future self.

If you have a provident fund from your employer or a pension fund, you’re one of the lucky ones.

Just don’t put all your hopes in those funds only. Perhaps buy yourself a diversified local and global tax-free ETF, and maybe a balanced fund retirement annuity that’s a good, diversified product to create your own pension fund.

Balanced funds are pretty balanced by nature they hold different asset classes like cash, bonds, property, equities, local, and offshore.

Not bad to hold one of those on the side to supplement your work provident fund, or if you don’t have a work provident fund, you can create your own.

In general, most experts recommend a 60% shares / 40% bonds split though this depends on your risk profile and age.

Just make sure you do your homework regarding fees, since most of these products are actively managed unlike the super-simple passive ETFs, which are low-cost by nature.

Retirement products and taxes

Retirement products are important for various reasons, particularly if one seeks to manage their tax burden.

Remember, “Give to Caesar what is his.”

Tax is inevitable but you can control how much you pay, somehow, if you contribute to a retirement fund like a retirement annuity.

If you’re happy with your provident fund at work, there’s no need to create another burden of a separate retirement fund. Rather, put your money into other discretionary investments ETFs, unit trusts, etc.

Since everyone is going crazy with crypto, just a word of caution: don’t hold more than 10% of your portfolio in crypto. Better safe than sorry.

You need to be diversified you can’t have all your money in one asset class.

Property and common sense

Property is good too, but don’t be like the property enthusiasts who have all their money in their residential property.

Actually, your residential property is not an investment if you’re not renting it out. Your home can be the worst financial decision if it’s the only asset you have.

Please don’t be emotional about this your house is a place to live, and it costs money to maintain: rates, levies, and all the other costs that come with homeownership.

Final word, spread those eggs in different baskets

This is diversification to me spread those eggs in different baskets, but don’t have too many baskets either, since that can backfire. You can’t carry several baskets comfortably.

Be sensible. Have different asset classes in your portfolio to weather volatility and market movements that’s how you manage risk.

Otherwise, enjoy the roller-coaster ride on your way to financial independence because that’s exactly how long-term investing feels at times.

Leave a comment