Maybe you are living right on the edge and not leaving any room for emergencies. They always say, save for those unknowns, since Murphy is already on his way as you are reading this.

When Murphy shows up: My car story

The other day, my car was due for a service. They phoned me to say that the car was ready for collection after the service. “Only a minor service,” they said. 😀

I thought, okay, maybe around R2,000. Nope, it’s R3,500. Fine, I can live with this amount, I thought.

But as I settled the bill and collected my keys, they added: “By the way, one of your back tyres is very smooth. Actually, you also need wheel alignment. Oh, and wait your other rear tyre has a nail. By the way, your battery failed the test; you should change it ASAP.”

The costs escalated from R3,500 to R9,000 two tyres, wheel alignment, and a new battery.

Another car story; this is even more serious than you think. It seems like Murphy likes to use cars often. A while back, while sitting in the gridlock traffic, I noticed massive smoke in front of my car. I thought What’s wrong with the vehicle in front of me? Why don’t people service their cars? I asked myself?

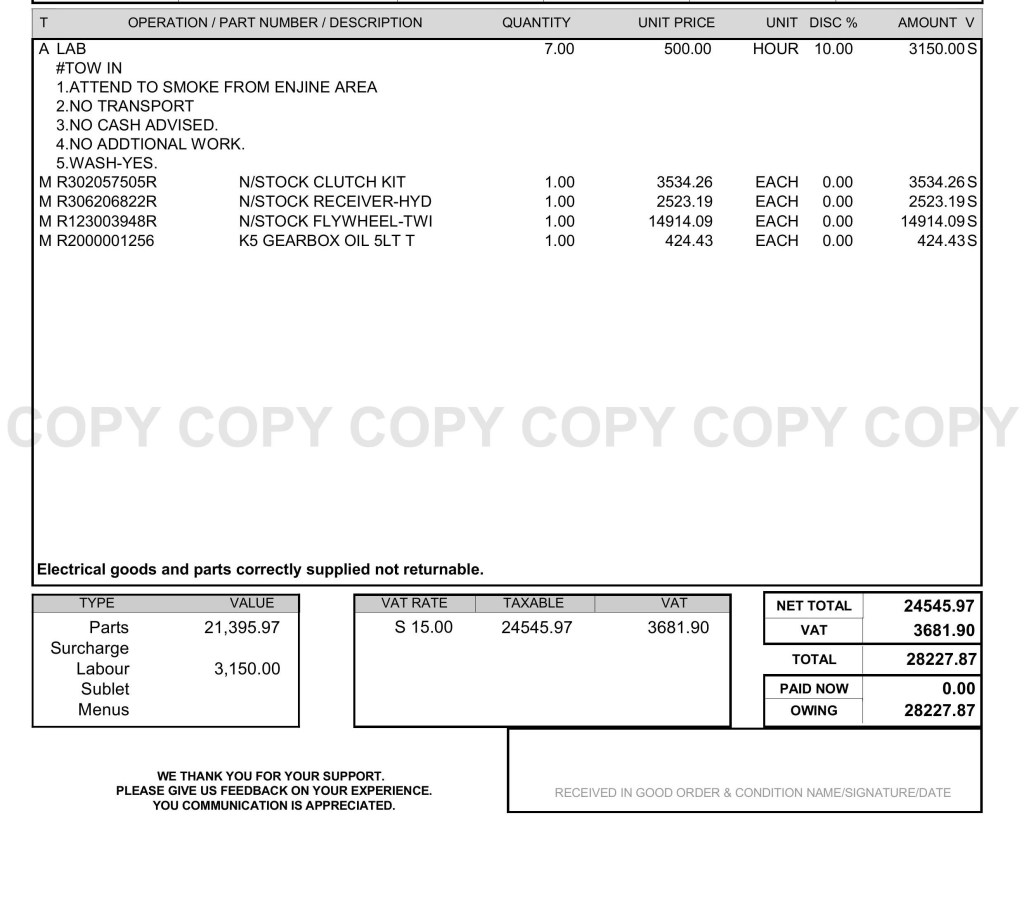

They are polluting the air. Oops, to my surprise, the smoke was coming from my bonnet. Long story short, apparently, I had burned my clutch, and guess what it cost me, R28227.87. Now that’s the mother of all Murphy. I have attached the invoice below in case you doubted me.

Welcome to adulting. Cars are expensive to maintain, particularly if one is not prepared. Truly Murphy’s Law at work: one thing after another.

Why an emergency fund matters

Since life is unpredictable, smart financial people like you and me should have a funded emergency fund to kick Murphy out of the way. At times, life feels smooth sailing, but don’t fall asleep at the wheel. Murphy, with the capital “M,” is always one event away.

Emergency savings are not there to prevent Murphy, but to push him away or at least soften his blows. Think of it like an electric fence: thieves don’t stay away because it exists, but they think twice before jumping in. Maybe Murphy does the same when you have savings.

But let’s be real: Murphy doesn’t care. He will still show up, whether you are prepared or not.

At most times, huge bills arrive just after you’ve finished paying another big one. That’s why this fund is called an emergency fund. You can never fully predict it.

Emergencies don’t announce themselves

The good old Book talks about how thieves come while we are sleeping, when we least expect them. Think of Murphy this way. Be prepared with an emergency fund buffer.

If you’re somewhat prepared, you won’t be shocked. You won’t derail your other financial plans like investing or saving for other goals.

Otherwise, if Murphy catches you unprepared, you panic. You might even phone a loan shark in confusion, or most of the time, max out that credit card or overdraft

An emergency fund turns a crisis into an inconvenience. Without it, your good intentions crumble. Remember the fight-or-flight response in emergencies, it’s hard to think straight.

And while flat tyres and leaking roofs hurt, the “mother of all Murphys” comes when your livelihood is compromised: a job layoff or a serious health issue. At those times, you realise you can’t repair a leaking roof in the middle of a storm, and no one is willing to give you a helping hand either.

Even having just three months of expenses saved gives you the calm and strength to process a layoff far better and work out plan B, than someone with no cash. Please, don’t be that dude who is unprepared who builds his house on the sand, disaster will be the result Murphy knows your name, and he strikes when you least expect him, and everything could fall apart.

Rules of the emergency fund

An emergency fund is a critical part of good personal finance management. Don’t cut corners. You need this shield just in case.

And remember: this is not holidaying money or iPhone money. If you lack discipline and are likely to spend it on a TV upgrade, Murphy will knock on your door right after and by then it will be too late.

So how much should you save? Experts often recommend three to six months of expenses. The exact amount depends on your situation; this is my opinion.

But here’s the trick: don’t keep this money in your checking account. You’ll be tempted to spend it on restaurants or random things. Remember, most of our decisions in life are driven by emotions. Rather save it in a:

- 24-hour notice deposit account, or

- Money market account.

And don’t invest your emergency fund it defeats the purpose if you need to sell investments in a hurry to pay for a flat tyre.

Yes, cash is king for emergencies. But don’t be over-cashed either, as you’ll lose out on investment growth. Strike a balance.

Be prepared, not surprised

Nothing in life is ever certain. Emergencies might be as small as a flat tyre, or as big as losing your job. You can’t be 100% prepared, but some preparation is always better than none.

An emergency fund prevents you from making desperate choices when life goes wrong.

And with the rise of fraud these days, don’t keep huge sums of cash in your Access Bank account. A notice deposit account is safer. Otherwise, internet fraudsters might clean out your debit account.

Final thoughts

Murphy is always around the corner, waiting. The question is: when he comes knocking, will you be ready?

Build your emergency fund. Treat it as your shield. It won’t stop Murphy from coming, but it will give you peace of mind when he does, and it softens Murphy’s blows.

Leave a comment