Net worth the first time I ever heard about NW was when I was reading an article in a financial magazine about the richest people in the world. This is one of those terms, in my opinion, that doesn’t get used much by ordinary people like you and me. This is our problem, as we often associate net worth with the wealthy of the world. You and I both have NW, and it’s time to take stock and check this magic number.

This number basically tells you whether you are going backwards or forward in your personal finance management. One’s net worth goes up or down depending on various factors it could be financial market movements, savings rates, taking on debt, or, at best, paying off debt.

If you could learn one thing after reading this article, please go and calculate your net worth. Yes, go and do the math after reading this article. Don’t worry, I will give you the equation it’s not hard math after all. Everyone has their unique net worth depending on their circumstances, which is why you should do your calculations. I am sorry if you don’t like math; there is no other way.

What is net worth?

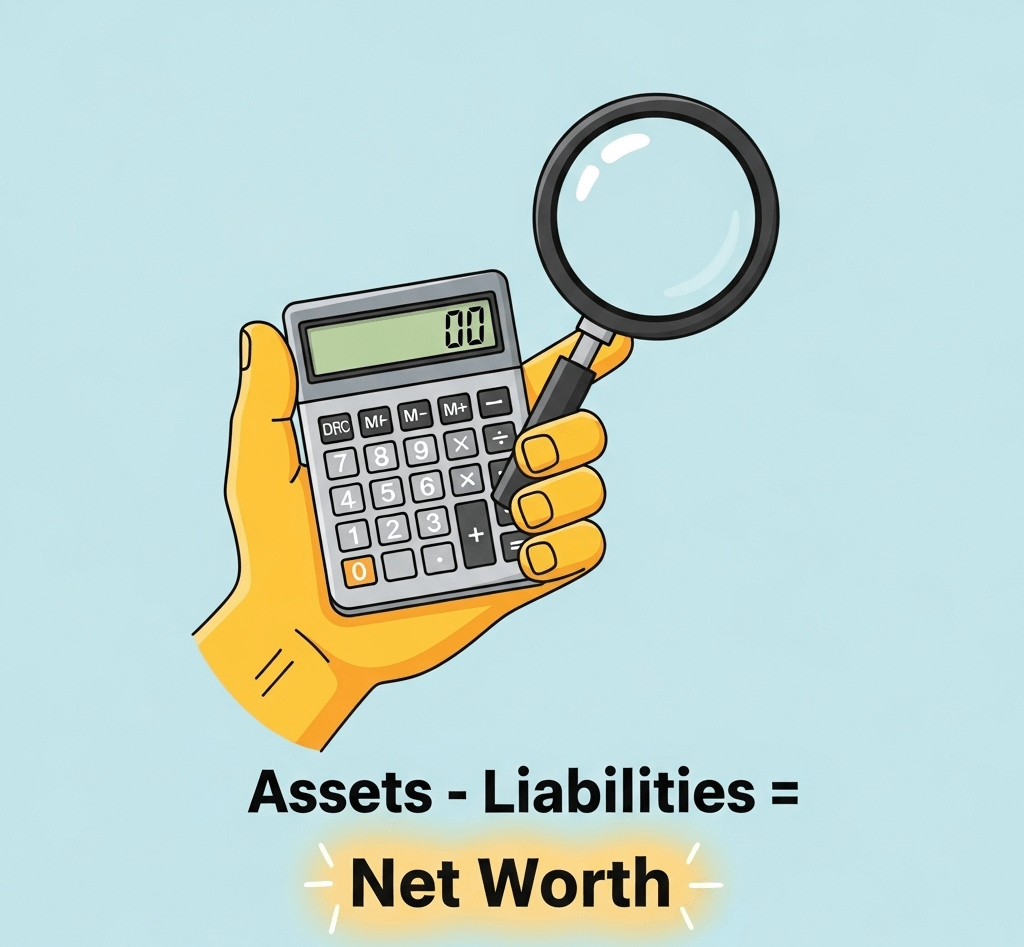

In short, net worth is what you own minus what you owe. In fancy financial terms, it means Assets minus Liabilities = Net Worth. For this exercise, we are going to talk about investible assets, although at times, people can include all sorts of things they own. Excuse me, we are not going to include your ridiculous painting hanging on your wall, which you are not sure how much it’s worth. Chill out, I understand your cousin said, you could cash in on the painting just for the sake of real assets, let’s not count the painting or your golf clubs in your garage, you have barely used.

Examples of Assets (What You Own)

- Retirement funds, e.g., Pension Funds, Provident Fund, Retirement Annuity, etc.

- Other investments: Tax-Free Savings Account, ETFs, Unit Trust, etc.

- Balance in your bank account

- Cash in your wallet and under the couch

- Property value

Examples of Liabilities (What You Owe)

- Home loan

- Personal loan

- Consumer debt: credit cards, store cards

- Car loan

- Student loan

Assets minus Liabilities = Net Worth

Now, add up your assets, subtract your liabilities, and there you have it that’s your net worth.

As explained above, that’s your financial net worth. Remember, your life is worth more than this number; this number is just the financial value of your real assets.

Where do we go from here? At times, your net worth might be negative if your liabilities are higher than your assets. If this is the case, don’t despair you can work your way out of the negative zone to zero. I’m told it’s a big deal to be on zero. Once you get to zero, you have created a margin to positively work your way up to the green number, which is your positive net worth.

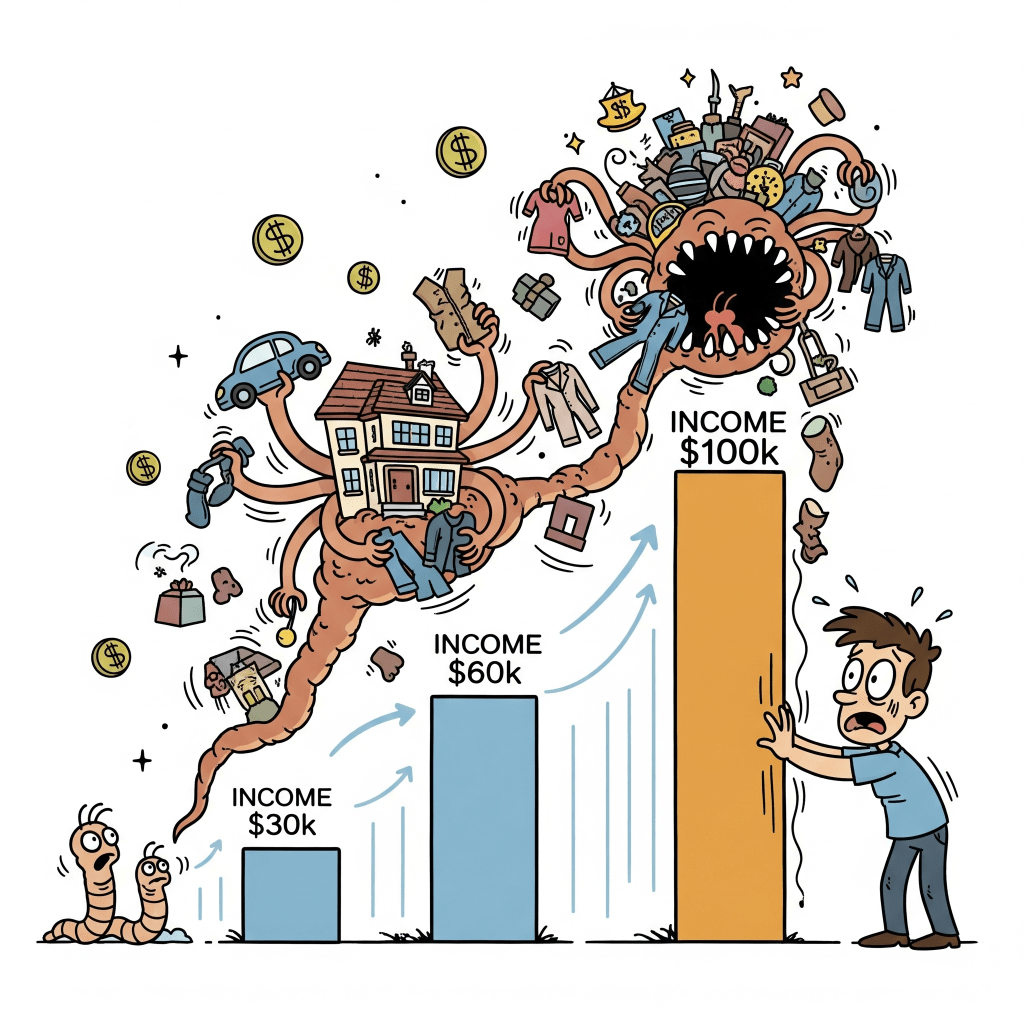

High net worth reflects diligent and disciplined saving and investing over time. We have to work on growing our net worth. When you receive a salary increase, you have to increase your savings too. We all start somewhere. If your net worth is shocking, don’t be shocked; one can improve this number over time. As your savings rate increases, your net worth should work its way up one month at a time.

Lifestyle Inflation

True story. I heard about someone who was earning R10 000 per month, and at this point in time, they didn’t own a car. They did well for themselves and managed a job upgrade in another company, and dramatically increased their salary to R20 000 per month. Good job, so they doubled their salary. Here is the financial tragedy part they suddenly went to finance and buy a brand-new car, not just a car, an SUV at an instalment of R10 000 per month, including insurance, etc.

At face value, you might reason and say they are moving forward in life. They went from carless to an SUV. The math, however, says the opposite: this individual is exactly back to a R10 000 salary, since the other R10 000 will go straight to finance the Lannie SUV. If you approach your finances this way, forget it your NW will never grow, ultimately meaning working longer and financial freedom is out of reach. Point to remember high salary doesn’t build you wealth, but what you keep and invest out of that salary does.

Lifestyle creep, as they call it in personal finance, is your real enemy. Does it mean never increase your lifestyle? Not at all. But be wise about it. Otherwise, you take all your increase to fund consumption and never grow your net worth.

The key is to fight those liabilities mercilessly and nurture the growth of your assets. Remember, the liabilities are not your friends they are bleeding your cash. Minimize or eliminate them; otherwise, they will eat your lunch right in front of your eyes.

So, in principle, liabilities eat your money, while assets multiply your money and eventually grow your net worth.

Next time you hear about net worth, don’t ignore the word like I did before, thinking it’s only for the Forbes list, but it’s for every individual who uses money. This magic NW is the one that banks, at times, work with if you want to borrow huge amounts for property purchases or even to start a business.

So, in financial terms, your worth is not based on the car you drive but on the investible assets you own not some shiny metal on four wheels. Ideally, calculate your net worth every 6 months or so and seek to improve this number over time.

Finally, don’t go about publishing your net worth

it’s personal finance for a reason. We are on a separate journey. Unless you are on the Forbes list, if so, you don’t need to tell us your net worth; we’ll read your name in the magazine.

Leave a comment