Time to talk shapes; don’t stress about it. It’s not as hard as it sounds.

There was always something about math that annoyed me: calculating, measuring, formulas… at least during my school years. I had a deep belief that math was hard. Funny how perceptions often shape our reality. In case you are wondering, confession time: I didn’t do well in maths at school. I had the potential, most definitely, though my limiting belief held me back; I couldn’t see beyond the curtain. Don’t worry about me, it turned out all fine!

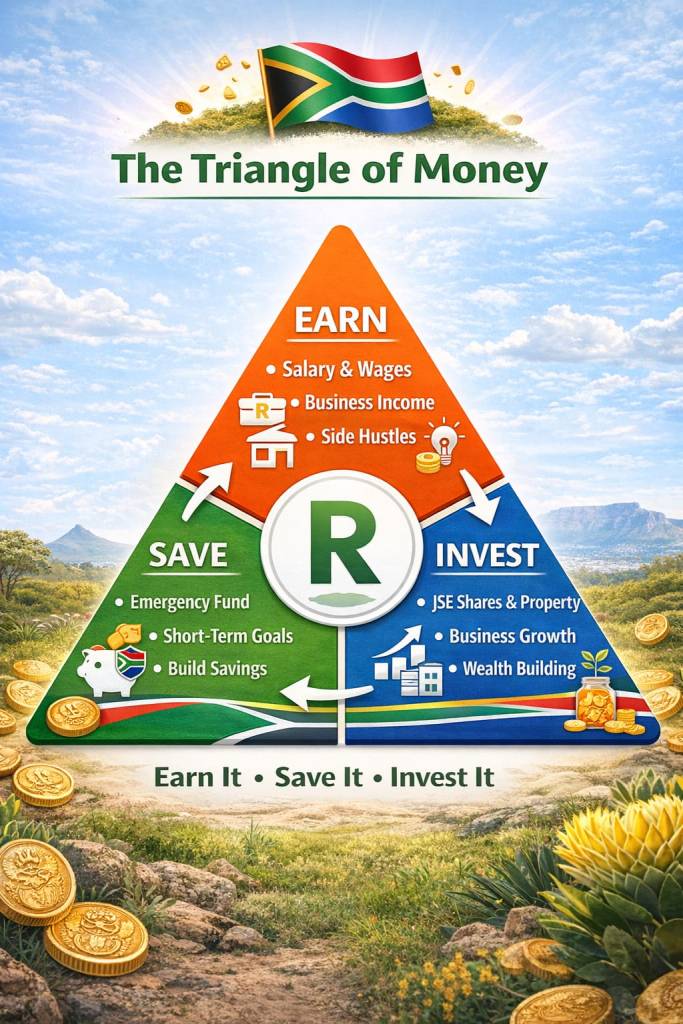

Why personal finance is like a triangle

So, let’s talk about the money triangle.

No calculations this time.

No need to take out your math set.

We won’t need measuring tools or projectors, just the triangle.

Triangles have three sides, and so does personal finance.

If you are to succeed on your money journey, you need to understand all three. Misunderstand even one side and tough times, my friend.

This triangle looks like this:

1. Income generation: The foundation of your financial journey

Earn is the very first side, and mostly what everyone knows about money.

You finish school, go to varsity, or perhaps straight to work if you are lucky. Jobs don’t come easily these days. Have you seen the number of LinkedIn profiles that are marked open to work? We’re not even talking about types of work yet, just work. Apparently, you need to know someone to get in, or know someone who knows someone; that’s being connected.

Ever become friendly with a stranger in a retail store, and they ask you for work? If not for themselves, then for a brother or sister. This is Africa; Next time I see you, I will give you my cousin’s CV.

You need to earn money first before anything else.

If you are not earning a salary or some form of income, wealth building is miles away, and financial independence is even further.

So, get yourself a job, possibly with a better salary too. You choose what “better” means. Obviously, it depends on lifestyle and cost of living. Some jobs are purely stepping stones. On a very minuscule income, financial freedom becomes extremely difficult; the math works against you.

Earn first. That’s the first muscle 💪 you should build.

And do not forget to settle debts before saving and investing. Most times, the cost of debt is higher than any investment return. Kill the fat before building the muscle; that’s what I mean.

2. Mastering the art of saving: Building your financial safety net

Saving is perhaps the hardest muscle to build; after earning, you need to graduate to saving.

Saving money is like building a six-pack. While most people can build biceps, triceps, and quads, only a few possess the discipline required to develop abs. Sit-ups, once in a while, will not help much.

Saving money is the most underrated discipline every adult should possess. It’s not about having enough money; it’s about saving what you already have.

Saving must be a priority, just like groceries and your airtime. Neglect this muscle, and you’ll be stuck forever.

Emergency funds, seeds, and survival

Saving is keeping the seeds.

Investing is planting seeds for the next harvest; that’s financial freedom.

An emergency fund is the harvest you can’t plant because you might need it today, tomorrow, or next week.

You can’t speed up the growing process when your kids are starving. Neither can you dig up seeds to prepare a meal you need right now. That’s the reason you require a what-if fund.

3. Investing 101: How to multiply wealth and beat inflation

Investing is the last part; this is the money multiplier.

Commonly known as making your money work for you:

Earning is working for money

Saving is keeping some of that money

Investing is assigning that money a task to earn more money, employing it to earn more money. Now that’s being your money boss.

Investing is hard, but not as hard as earning or saving, at least.

How investing multiplies wealth

Again, think of it this way:

Earning is gathering

Saving is keeping

Investing is multiplying, even quadrupling, when the ship catches the wind; it’s unstoppable.

There are many investment strategies. My simple suggestion: low-fee passive index funds and ETFs, since they spread risk and grow steadily. That’s a solid starting point. And of course, don’t forget the retirement fund; the old dude is counting on you.

Tax-free savings accounts also form part of that long-term retirement picture.

Why your primary residence isn’t a traditional investment

Property and businesses can be investments too, but usually not your residential property. That thing eats money more than it makes.

Leaking bathroom pipes in the wall.

Moisture showing up where it shouldn’t.

Missing roof tiles after heavy wind or rain.

The kitchen sink is leaking. Call the plumber before the cupboards are ruined.

This explains why your home is not an investment. There are many hidden costs associated with owning your mansion.

Final thoughts: Keeping your money triangle strong

In simple terms, earning money is like qualifying for the Olympics: hard on its own. Saving is like winning bronze. Investing is the gold medal; only a few stand on the centre podium.

I’ve never been to the Olympics, and I’m pretty sure I never will be, maybe just to watch others compete.

Observing this triad of the money triangle is necessary for anyone serious about building wealth. Neglect any side and, in my humble opinion, you’ll get an F on your money exam. What are you doing today to ensure that your money triangle is steady and secure?

Earn millions, but fail to save and invest; nothing else matters.

Save but fail to invest, and inflation will beat you to your money. That invisible monster feeds on your cash right in front of your eyes, obviously, silently. It’s an invisible ghost.

Only investing can kick inflation away.

When you practice all three sides of the triangle, you set your money story.

That, my friend, is being an adult in my world. Now, what’s one step you can take today to strengthen your money triangle?

Leave a comment