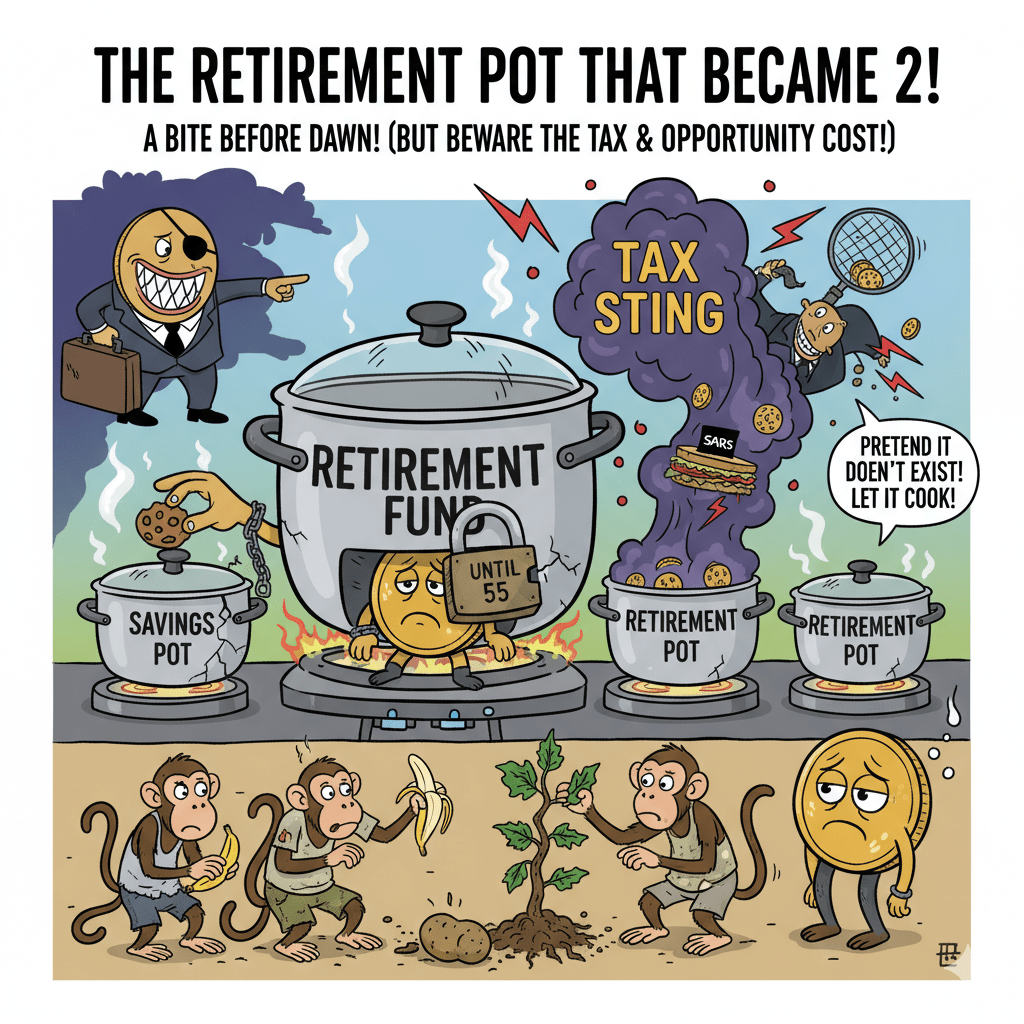

Locked-up future lunch while folks are starving today, tough times were. Your money was locked up and only accessible after 55 years. This was the problem with South Africa’s retirement funds Provident funds, Pension funds, and Retirement Annuities.

After much deliberation and debate over retirement funds, and weighing the difficulties of people resigning to access their lunch before sunrise, the government finally gave people the go-ahead to take a bite of the sandwich early before dawn.

⚠️ Caution, this bite comes with a huge tax sting.

A bite before dawn

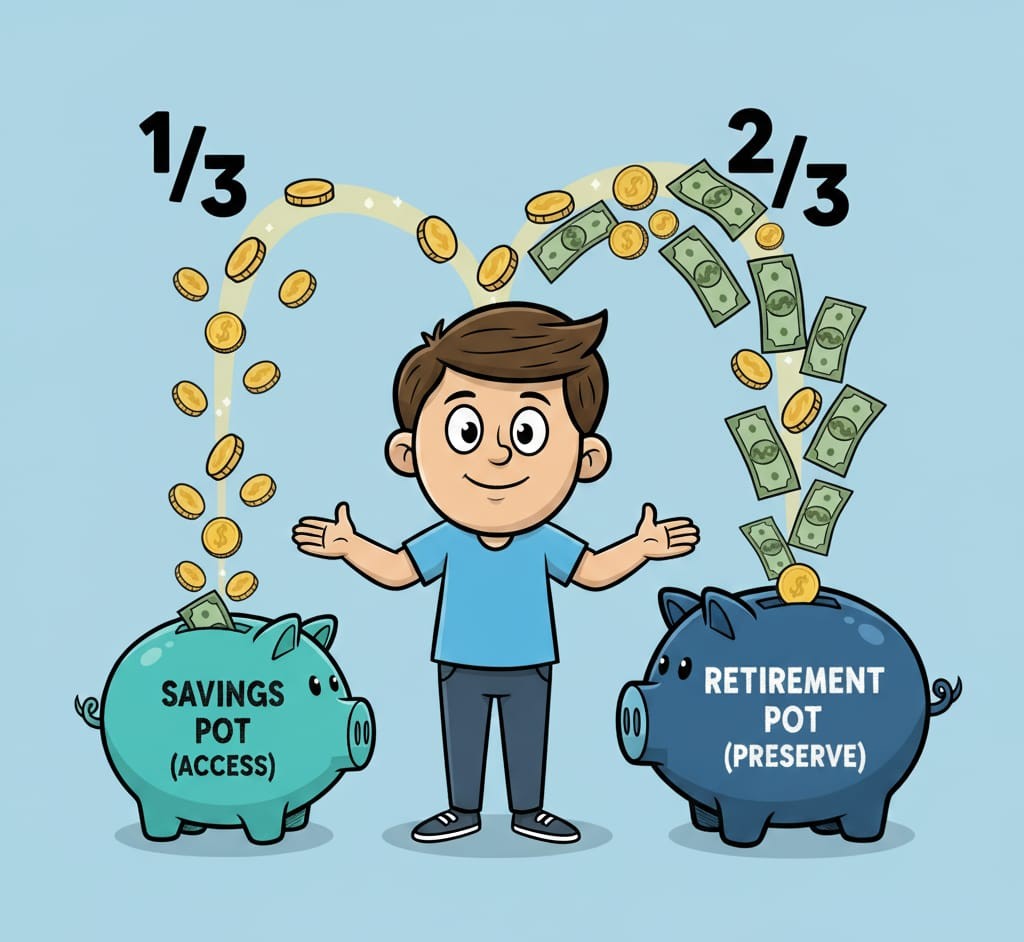

Since you and I are emotionally driven and tend to have a YOLO mindset, we are still not allowed to touch the whole lunch, but only 1/3. The other 2/3, which make up the second pot, is still locked up until we are 55 years old.

Actually, in some cases, there are 3 pots:

- Savings

- Retirement

- Vested

In case you are wondering what the vested pot is, it’s the pot containing contributions before the new system came into effect.

I wonder who is cooking these pots? Why do we even use the analogy of pots in the first place? Perhaps it’s because those investments are still cooking and not yet ready to be served, the plates are not yet served, chill out for a little while.

However, it seems the government has finally behaved like the parent of a toddler who gave in after being nagged for an extra cookie and eventually gives in, allowing you to have a 1/3 bite in your savings pot.

Only bite if you’re really hungry don’t just bite for the sake of it. Remember, it’s not the government’s money at risk; it’s your future self you’ll be taking from if you choose to pull money from your retirement savings pot.

In fact, the government gets a bigger portion if you tap into the savings pot early, as you are taxed at your current marginal rate. Realistically, you should only access the savings pot if it’s a matter of life or death, that is, really a serious emergency, not a holiday to Sun City.

Side note: Be cautious when visiting Sun City. Stay away from the casino. Actually, the hard reality is that these days, physical casinos are not the only temptation; people can also engage in sports betting on their phones. Thanks to technology, casinos are now in our pockets.

Example, the tax sting

Let’s say you earn R20,000 a month and you decide to withdraw R10,000 from your savings pot.

- Because this withdrawal is taxed at your marginal tax rate, it’s added to your income for that year.

- If your marginal tax rate is 31%, SARS takes R3,100 immediately.

- You don’t walk away with R10,000. You only get R6,900 in your pocket; not only that, this amount would be less since you would also need to pay the fund administration withdrawal fees.

👉 Almost a third is gone before the deposit SMS tone rings in your phone.

One cookie is still one whole

What’s important to note is that your retirement fund still makes up the whole. Splitting it into 2 doesn’t make it bigger; the 2 pots together still equal the original cookie. It’s just divided, please resist taking a bite out of your savings pot.

Borrowing from yourself

If you are stuck between a rock and a hard place, as they say, like my colleague who once asked me:

Is it better to borrow from the loan shark or from the savings pot?

I suggest it’s far better to borrow from your future self by accessing the savings pot than to entertain the loan shark, it is a shark after all, we know who would end up bleeding or even dead. Important insight: Please do not touch your retirement savings every year. The more you bite from that pot, the more your future self will starve, and you’ll be the one to blame.

There is also a huge opportunity cost of withdrawing money early, since you’ll miss out on potential compound interest for future growth.

Example – The opportunity cost

Now, imagine that instead of withdrawing R10,000 today, you left it in your pot to cook for 20 years at an average annual return of 7%.

- In 20 years, that R10,000 would simmer and grow to around R38,696.

- By withdrawing now, you’re not just losing R3,100 in tax you’re losing nearly R28,000 in future growth. This is an astronomical opportunity cost to be entertained; ask the economist, and they will agree with me.

In other words, today’s “small snack” could have been a full meal (with cheese cake for dessert 🍰) for your future old self to indulge in.

Accessing your savings pot early is not recommended in most cases, but remember Mashonisa is not your cousin. Please don’t even talk to him. At least your future self is related to you and understands you in some way 😜.

Remember this: the older you get, the less you care about the tender fillet steak you ate yesterday. That’s why it’s not wise to use his money today for a restaurant meal either. Your future old self is more worried about their well-being.

Pretend savings pot doesn’t exist

What am I saying here? Only touch the savings pot in extreme cases. Otherwise, you’ll defeat the whole purpose of retirement savings in the first place.

You and I are better off pretending that the 2-pot system doesn’t exist treat your retirement contributions as one whole, and your future self will be grateful. Instead, build a separate emergency fund just in case your tyre bursts.

The biggest temptation lies in the availability of the savings pot. Just because you’re allowed to access it once a year doesn’t mean you should.

Marshmallows and monkey brains

In a way, this feels like the Marshmallow Study by Stanford University in the 1960s: the Delayed gratification conundrum, eat one marshmallow today or save it and have more in the future. Most people would rather enjoy the fluffy sugar today.

It’s not surprising at all, since humans are complex creatures, and emotions play a huge part in who we are. You and I should learn to rein in instant gratification and give our savings pot enough time to cook and mature if we are to win the financial independence game.

Hard reality, sometimes, though, we act like monkeys 🐒.

True story: I grew a potato plant in my garden. It grew big, lush, and green, but wasn’t yet mature, and no potatoes were ready. One day, while I was away, a troop of monkeys came and uprooted the entire plant looking for potatoes. Only roots nothing else, since the potato plant was not ready, you see, we as humans are not so good with our value judgments most of the time.

Please don’t reason like these cousin creatures of ours.

Have you also noticed how monkeys often throw fruit on the floor, barely eating it? Why? I often wonder. But the truth is, you and I can behave the same way at times. Just don’t behave like this with your retirement savings, or you could retire broke and miserable. At least monkeys have the whole forest to feed them, or they could still steal your bananas in your home.

The technical side

Back to the technicalities of the 2-pot system:

- When you retire, you can access the Savings Pot as cash.

- The Retirement Pot and Vested Pot must be used to buy you an annuity meaning you only access them as monthly income.

Some real numbers close to home: according to SARS, since the inception of the 2-pot system, that is, September 2024, the amount withdrawn is estimated to be R57 billion as of July 2025.

And here’s the kicker: SARS cashed in its tax portion first, before you get your share. Talk about the big brother beating you to your lunch first before you 🤔.

If you do the math, it doesn’t make sense to access your savings pot early, because you’re still at a higher tax rate than you’ll likely be at retirement. SARS won’t mind, though they get their share first, it’s a win-lose scenario for you.

Key takeaway

The savings pot might look tempting, but it’s not free money. It’s your future lunch, not today’s snack.

If you can, leave it alone, let it cook, and give your future self something to smile about. Let compound interest simmer long enough to serve you a buffet. In fact, if that meat cooks long enough will be falling off the bone by the time you pull out your savings pot in retirement.

Leave a comment