Budget forms a critical part of personal finance. Don’t treat it as a swear word, although they might seem like one. Most people avoid budget as if it were a swear word.

We live in undoubtedly over-marketed and highly over-advertised times. Without a blueprint for intentional living, as I call it, impulse buying will ruin your financial life. Budgets are not as restrictive as most people think 🤔They are freeing, empowering, and can be fun too.

You see, if you religiously follow a budget, you get to spend money on things you enjoy, too, without feeling guilty. It’s not all about pinching pennies, but about prioritising what’s important to you. I must admit it can be boring and monotonous at first, but once you get the hang of things, you will enjoy following this blueprint, and you can build an exciting life too.

Personally, at most times in my adult life, I viewed budgeting as restrictive, almost like a diet of some sort. Not sure where this thinking comes from, must be one of those money psychology mindsets. Everyone has their own money bias rooted in their worldview, I’m told.

Perhaps budgeting is mostly avoided because of the discipline part. This is the sweet spot you should somehow embrace as a way of a healthy life, since it’s very unlikely to be successful at anything in life without discipline.

A blueprint at work

Let’s say we want to build a cool building structure, one of those you see on HGTV. We don’t just start digging foundations. Ask a builder, and he’ll tell you: we need a blueprint, sometimes known as a plan. This is the drawing of our cool building on paper, first, before we start building it.

Such is a budget, a blueprint for intentional living. Otherwise, we’ll sleepwalk through life, spending money aimlessly. The marketers know this. That’s why they bombard us with adverts all the time.

To resist these hungry sharks, one needs discipline, and a budget forms part of that. Otherwise, the sharks will feast on your wallet forever.

Reading the blueprint is boring, but essential

Years ago, I worked with a builder soon after high school, at around 17 years old. It frustrated me walking around this old dude as his assistant on the building site while he studied and read the house plan on a giant paper, you know, those kinds of paper that are hard to fold, same type as a physical map before electronic GPS.

Imagine the frustration of folding and opening this thing while walking around the site 😀. I just wanted to get to the building part.

Not so fast, we need to study the blueprint first.

If you are serious about financial freedom, you need a blueprint ASAP, and that plan is the budget.

Good news: you don’t have to walk around with a giant paper difficult to fold. But you still need a blueprint. A budget is empowering in the sense that you will save, invest, and spend money purposefully. It is a guide on how you will spend your cash when it hits your account.

Are you tired of not knowing where your money is going? Create a plan and follow that plan intently, and soon you will know where your money 💰 is going.

All line items in the budget must be realistic and show the different categories, for example. Following this plan will eventually become autopilot, and soon you will do it with little effort.

These 3 parts should influence your budget plan

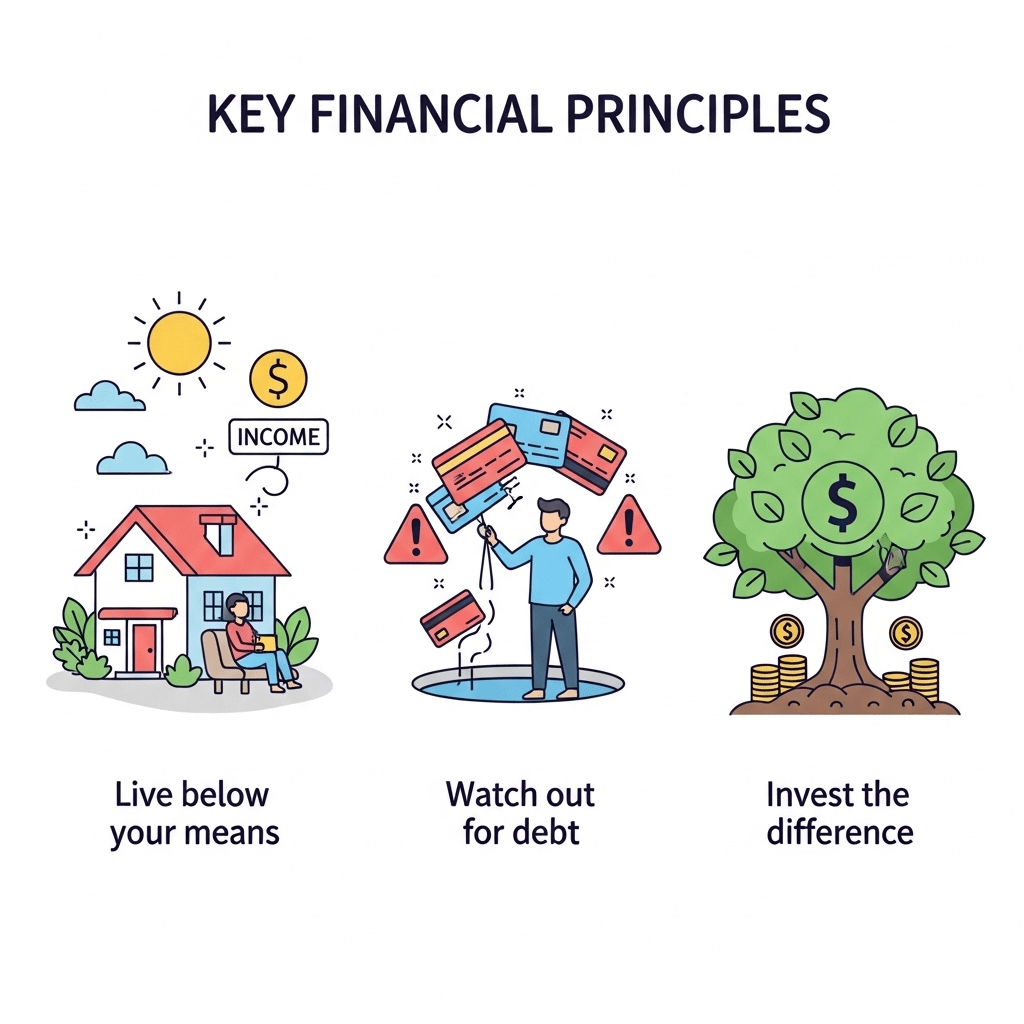

1. Live below your means

Living below your means, learning to live on less money than you make.

If you follow the herd, you will spend everything that comes in without allowing yourself room to grow savings. I know it’s tight, we all live in South Africa; however, you need to decide what’s important to you and learn to live on less than you make.

Since resources are limited, we must pick and choose which are priority needs and wants, for example.

Side note: Take-away pizza every day of the week is not a need. If it is once a week or so, it’s understandable but not every day. You choose what makes sense for you: takeaways every day of the week, or time freedom way before you are 65. It’s up to you to make that judgment.

I’m sure you get the idea it’s okay to treat yourself occasionally, but you can’t do that at the expense of your financial freedom.

It’s way cheaper to braai your rump steak at home compared to a takeaway steak, trust me, I did the numbers. If you spend everything you make, you will never retire.

2. Watch out 😉the debt monster

Debt has the potential to prevent you from saving and investing altogether. It’s bad enough to spend all your money without saving, let alone to spend over and above your salary in the form of debt repayments and interest.

If you don’t control debt, debt will control you. You become a slave to your salary and your job. God forbid if you lose your job, you are finished.

From time to time, we do use debt, but be very careful that it doesn’t spiral out of control. Be particularly aware of consumer debt, such as credit cards and personal loans.

If a huge portion of your money is going toward debt repayment, you compromise your potential to save and invest. This is one of those personal finance areas you must tread very carefully, otherwise you end up working for banks and moneylenders. The wise saying from the good old book of wisdom states that “the borrower is a slave to the lender.” You choose which one you want to be.

Enough of the lecture, control your money. Don’t work for lenders, and don’t be enslaved by your money.

3. Invest the difference

Investing should be a priority if you are serious about time freedom. This is the magic phase when you make your money work for you; at times, your money can work harder than you do, even when you are sleeping.

Don’t invest what is left; invest first and spend what is left. The common mentality says spend first and at last look for what’s left and somehow try to invest that. If you follow this way of thinking, you will not make it to financial freedom. You and I should do the opposite since we need to get our freedom soon.

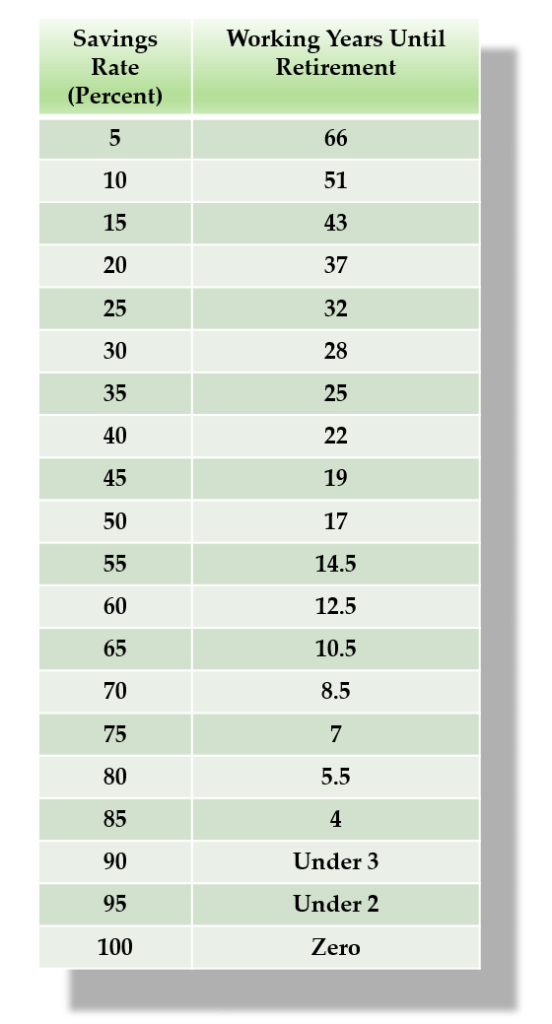

Bonus: What’s your savings rate?

In closing, let’s talk about savings rates this is the percentage of your salary you are saving and investing each month toward your financial freedom.

Smart people did the math. Apparently, the bigger your savings rate, the earlier you will reach freedom.

Example: How to Calculate Your Savings Rate

If you are saving and investing R2000 per month from a R20,000 salary:

R2000 ÷ R20,000 × 100 = 10%

Your savings rate is 10%.

At this rate, it will take you some 51 years to reach financial freedom. That’s an awful lot of time. It’s okay if you desire to work 51 years, not me!

Final thoughts

Check these numbers below from the famous, cool guy, Mr. Money Mustache. I’ll link his blog below if you’d like to dig deeper. Meanwhile, reflect on where you are based on your current savings rate and how long it might take you to reach your freedom. Please embrace the word budget it’s not a swear word that you should avoid.

Leave a comment